Copper, iron ore price rally adds $250bn to Top 50 mining companies

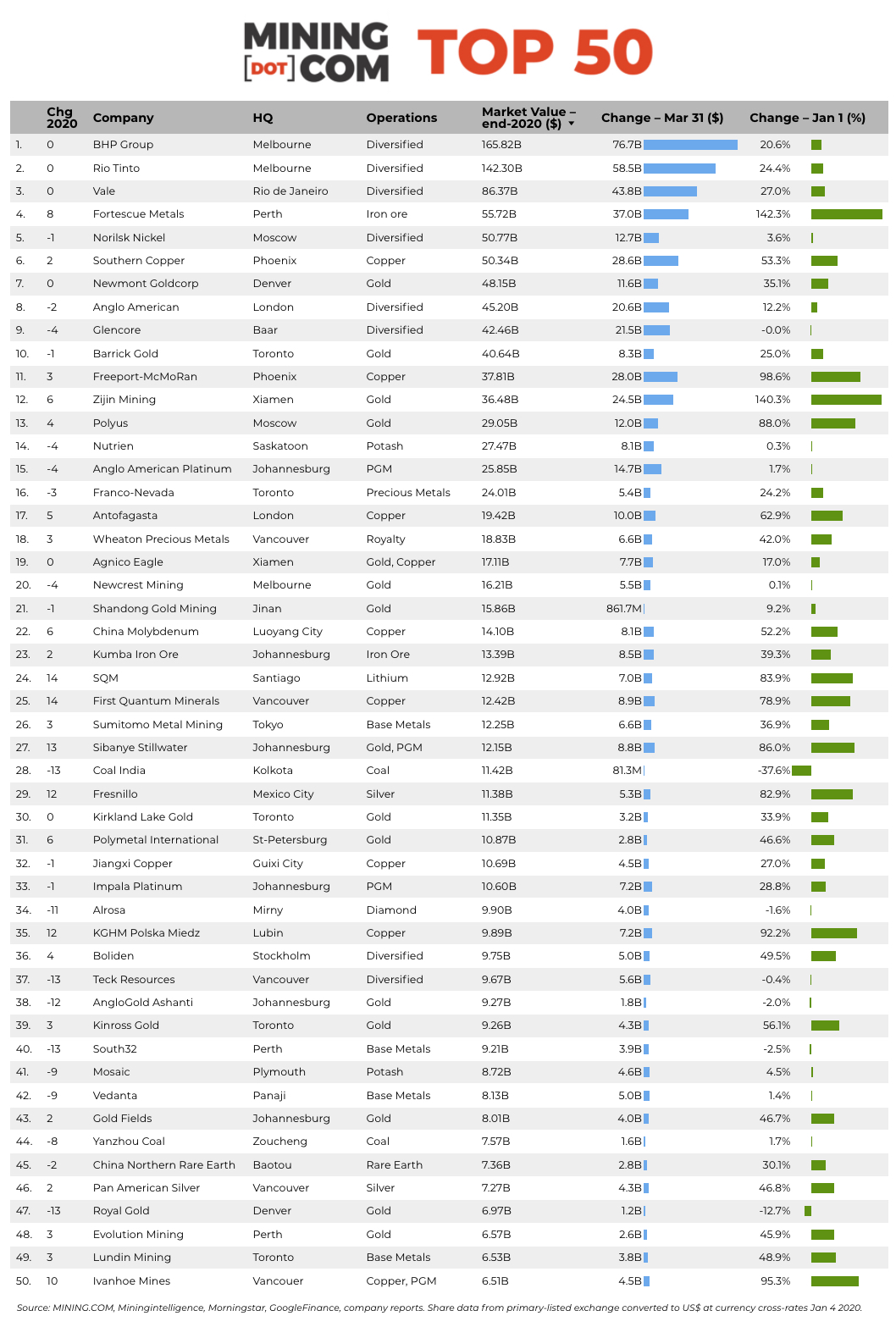

Propelled by a fourth-quarter rally in copper and iron ore prices, MINING.COM’s ranking of the world’s 50 most valuable mining companies jumps to a new record high of $1.3 trillion by year’s end.

The Top 50 most valuable mining companies added $250 billion in market capitalization over the three months to end December thanks to surging base metal and iron ore prices, and precious metals markets holding onto most of their 2020 gains.

Measured from the height of the pandemic in March-April, the MINING.COM TOP 50* has now recovered by $580 billion amid predictions of a post-pandemic supercycle in commodities demand thanks to construction and green infrastructure spending not only in China but also in the US and many parts of the developed and emerging world.

Iron ore price lit a fire under the top 4 producers, with a strengthening currency further boosting BHP, Rio Tinto, and Fortescue’s US dollar value during the year.

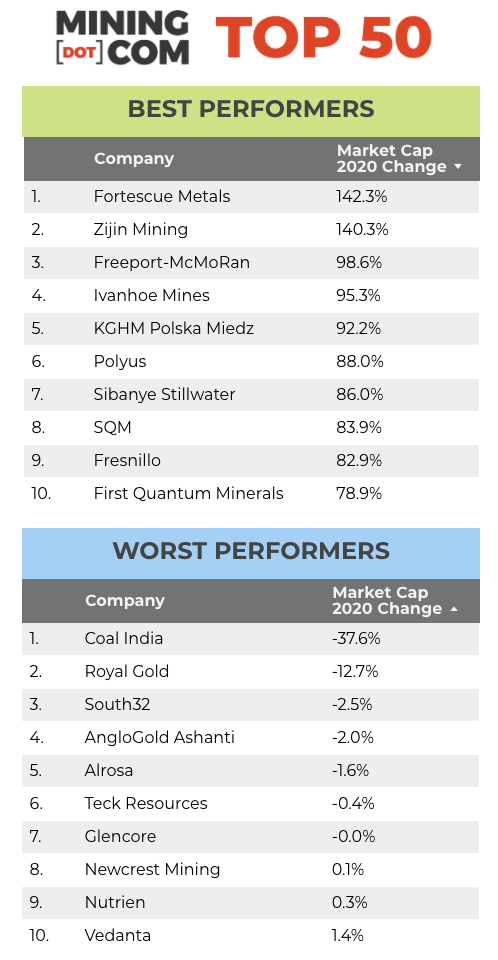

Fortescue Metals Group was the best overall performer in 2020, climbing to number 4 after starting the year outside the top 10. US iron ore producer Cleveland Cliffs managed to climb 18 spots but fell just short of the ranking at position number 53.

Gold’s relative underperformance during the quarter saw two mid-tier producers – B2Gold and Yamana Gold – fall out of the top 50 at year-end and replaced by Lundin Mining and Ivanhoe Mines. Once Endeavour (which also absorbed Samafo this year) and Teranga close their combination, the merged entity would stand a good chance of entering the Top 50.

Base metal miners stormed the rankings towards the end of the year, and Ivanhoe becomes the first non-producing company to rank among the Top 50 and joins other copper companies on the best performing list, notably Freeport McMoRan and KGHM.

FCX doubled over the course of the year, but is up an astonishing 400% from its covid-lows in March. KGHM briefly dropped out of the Top 50 at the end of the first quarter but is now back at no 35.

Quantum Minerals shares the honor of fastest climber this year with lithium miner SQM – while copper has rallied hard, the lithium market has at least put the worst behind it.

Click on image below for full table:

* Notes:

As with any ranking, criteria for inclusion are contentious. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information.

That, of course, excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining, which owns the world’s largest gold mine, Eurochem, a major potash firm, trader Trafigura, top uranium producer Kazatomprom (partially listed on the LSE, but with only an estimated market value) and numerous entities in China and developing countries around the world.

Another central criterion was the depth of involvement in the industry before an enterprise can rightfully be called a mining company.

For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or not even warrant a seat on the board?

This is a common structure in Asia, and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec.

Levels of operational involvement and size of shareholding were central considerations.

Do streaming and royalty companies that receive metals from mining operations without shareholding qualify, or are they just specialized financing vehicles? We included Franco Nevada, Royal Gold and Wheaton Precious Metals.

What about diversified companies such as BHP or Teck with substantial oil and gas assets? Or oil sands companies that use conventional mining methods to extract bitumen, for that matter?

Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy where power, ports and railways make up a large portion of revenues pose a problem as do diversified companies such as Anglo American with separately listed majority-owned subsidiaries. We’ve included Angloplat in the ranking, as well as Kumba Iron Ore.

Chemical companies are also problematic – should Albemarle not be ranked because its potash and lithium operations are such a small part of its overall revenues? The same issue applied to FMC before it spun off its lithium business.

Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and others.

Head office refers to operational headquarters wherever applicable, for example BHP and Rio Tinto are shown as Melbourne, Australia, but Antofagasta is the exception that proves the rule. We consider the company’s HQ to be in London, where it has been listed since the late 1800s.

Trading data are from primary listing exchange and currency cross-rates at the date of publication. Market capitalization calculated at primary exchange, where applicable from total shares outstanding, not only free-floating shares.

source: Mining.com

![]()